Simulates a (continuous time) random walk as a Brownian drift. For mu = 0 the random walk is unbiased, otherwise it is biased.

Value

A list with elements t and y. t is a duplicate of the input parameter and is the times at which the random walk is evaluated. y are the values of the random walk at said times. Output list is of S3 class timelist (inherits from list) and can thus be plotted directly using plot, see ?admtools::plot.timelist

See also

stasis()andornstein_uhlenbeck()to simulate other modes of evolutionrandom_walk_sl()to simulate random walk on specimen level - for usage in conjunction with thepaleoTSpackage

Examples

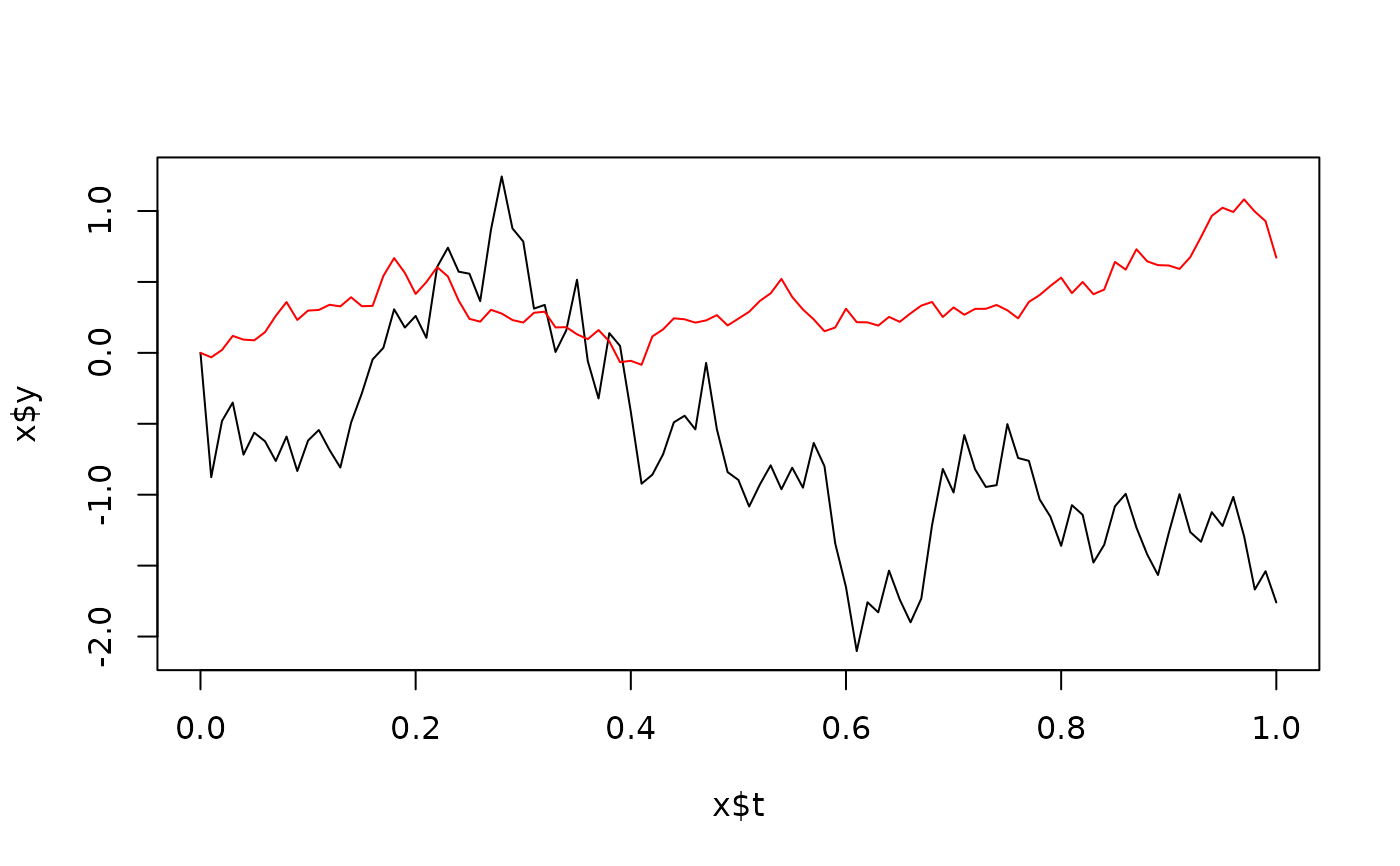

library("admtools") # required for plotting of results

t = seq(0, 1, by = 0.01)

l = random_walk(t, sigma = 3) # high variability, no direction

plot(l, type = "l")

l2 = random_walk(t, mu = 1) # low variabliity, increasing trend

lines(l2$t, l2$y, col = "red")